If you’ve ever wondered how personal checks fit into today’s fast-paced, digital payment world, you’re not alone. Despite the rise of mobile wallets and instant transfers, personal checks remain a surprisingly reliable way to handle large payments, avoid hidden fees, and maintain control over your finances. In this guide, you’ll discover what personal checks really are, why they still matter, and how you can use them smartly—whether for rent, bills, or international transactions. Ready to unlock the power of this classic payment tool? Let’s get started.

What Exactly Is a Personal Check?

A personal check is a written, dated, and signed document that instructs your bank to pay a specific amount of money to a named person or entity. It’s a simple and trusted payment method that lets you pay bills, rent, or transfer funds without using cash.

Key Components of a Personal Check

Every personal check includes several important parts:

- Date: When the check is written.

- Payee: The person or business receiving the money.

- Amount: Both numeric and written forms to avoid confusion.

- Signature: Your authorization to release funds.

- Memo: Optional note explaining the purpose of payment.

- Bank details: Your bank’s name, branch, and routing information.

Types of Personal Checks

There are different types of personal checks you might encounter:

- Cashier’s checks: Guaranteed by the bank, often used for large payments.

- Transfer checks: Used to move money between accounts.

- Ordinary checks: The most common, payable to a named person or company.

- Crossed checks: Marked with two parallel lines, making them payable only through a bank account for extra security.

A Brief History of Personal Checks

Personal checks have roots in centuries-old paper commerce, evolving from simple promissory notes to the secure, reliable payment tools we use today. While digital payments are on the rise, personal checks still play an important role in many everyday financial transactions due to their traceability and convenience.

The Step-by-Step Process: How to Open and Manage a Personal Check Account

Opening a personal check account is straightforward if you know the basics. Here’s what you need to keep in mind:

Eligibility and Requirements

- Minimum deposit: Most banks require a small initial deposit, usually between $100 and $500.

- ID verification: Be ready to provide valid ID like a passport or national ID card, proof of address, and sometimes a tax number.

Choosing the Right Bank

- Look for low or no fees on monthly maintenance and check orders.

- Consider easy access through local branches and ATMs.

- Check if the bank offers mobile banking apps that let you track your balance, get alerts, and even deposit checks digitally.

Account Setup Process

- Apply online or visit a branch. Online applications are often quicker and more convenient.

- Provide all personal details and documents requested.

- Once approved, you can request your checkbook to be mailed or picked up.

Managing Your Personal Check Account

- Keep track of your spending using your bank’s online tools or budgeting apps.

- Set up fraud alerts to get notified of suspicious transactions.

- Regularly review your bank statements to catch any unauthorized activity early.

By following these steps, you’ll have a well-managed personal check account that suits your daily needs and keeps your money safe.

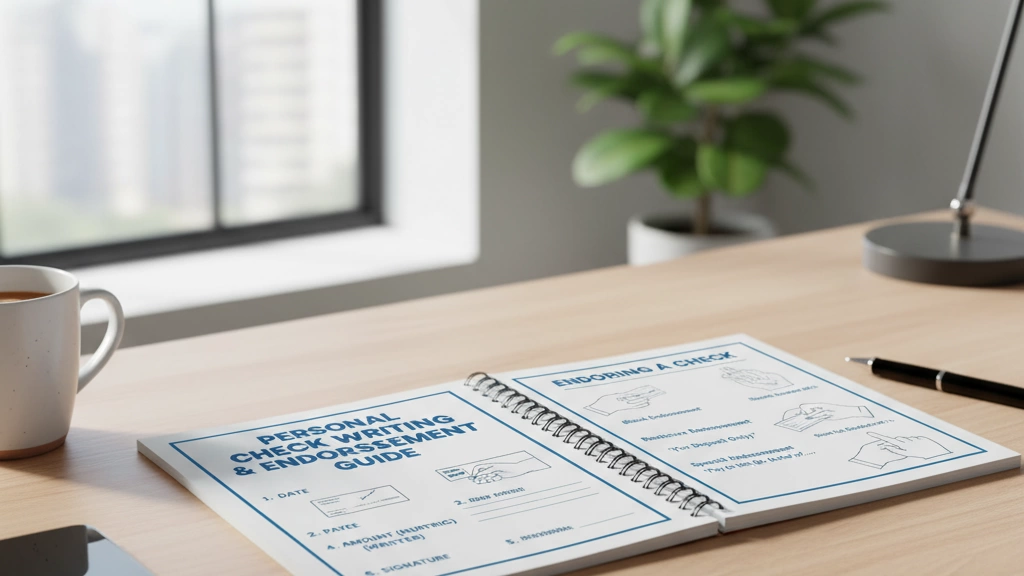

Mastering the Art of Writing and Endorsing Personal Checks

Writing a personal check might seem old-school, but getting it right is crucial for smooth payments. Here’s how to fill out a (personal check) properly and avoid common slip-ups:

Filling Out a Personal Check Correctly

- Date: Write today’s date clearly in the date line.

- Payee: Write the full name of the person or company receiving the money.

- Amount in Numbers: Fill in the amount in the small box (e.g., “125.50”).

- Amount in Words: Spell out the total amount clearly (e.g., “One hundred twenty-five dollars and 50/100”).

- Signature: Sign your name exactly as registered with your bank.

- Memo (optional): Use this space to note the purpose, like “Rent April” or “Invoice 1234.”

Common mistakes include mismatched amounts, missing signatures, or unclear handwriting — all risks for bounced checks or delays.

Types of Endorsements for Personal Checks

When you receive a check, you need to endorse it on the back before cashing or depositing it. Here are the endorsement types:

- Blank Endorsement: Just sign your name. Simple, but risky if lost – anyone can cash it.

- Restrictive Endorsement: Add “For deposit only” plus your signature to keep it secure.

- Third-Party Endorsement: Sign and write “Pay to the order of [Name]” if you want to transfer it, but be careful as many banks don’t accept third-party checks.

Check Security Best Practices

- Ink Choices: Always use a pen with permanent, dark ink (blue or black) to prevent alterations.

- Voiding Checks: If you make a mistake, write “VOID” across the check and keep it for your records.

- Keep Checkbooks Safe: Store your checkbook where others cannot access it to avoid fraud.

Real-Life Payment Scenarios

Here’s how checks come in handy:

- Paying your landlord for rent, writing clear purpose in the memo.

- Settling contractor bills by endorsing checks properly.

- Sending medical bill payments by mail, ensuring the check is signed and dated.

Mastering these steps will make your personal checking account smoother and more secure, whether for daily use or occasional big payments.

Where and When to Use Personal Checks: Practical Applications

Personal checks (个人支票) still have a place in everyday life, especially when cash or digital payments aren’t the best fit. Here’s where they come in handy:

Common Uses of Personal Checks

- Rent and Fees: Many landlords and property managers still prefer checks for rent payments or monthly fees. It’s a reliable paper trail both sides appreciate.

- Medical Bills: Some clinics or doctors accept personal checks, especially in smaller towns or clinics that don’t take cards.

- Contractors and Services: Paying contractors, repairmen, or freelancers with a check is common when you want a clear payment record.

- Schools and Clubs: For tuition, membership dues, or donations, checks offer a secure way to handle money without digital platforms.

Benefits When Traveling or Dealing Internationally

- Using personal checks abroad is less common but still useful in some countries where card acceptance is low.

- Personal checks avoid ATM or credit card fees and provide proof of payment without sharing sensitive card data.

- Remember to verify if the receiving bank accepts foreign personal checks.

Niche Roles of Personal Checks

- Identity Proof: Writing a check can sometimes serve as ID verification for certain transactions or registrations.

- Low-Tech Transactions: In places or situations without reliable internet or mobile payments, checks are a simple fallback.

Limitations and Alternatives

- Personal checks take time to clear, which slows down payment.

- Not widely accepted everywhere, especially with younger generations preferring digital methods.

- Alternatives like ACH Transfers: Electronic ACH payments are faster, more secure, and increasingly replacing personal checks for recurring bills and payroll.

In , personal checks remain useful in specific situations — mostly where a paper trail is preferred or digital options are limited. But knowing when to use them versus faster alternatives helps keep your finances smooth and secure.

Navigating Security and Risks: Protecting Your Finances with Personal Checks

Using comes with security concerns, but a few smart steps can keep your money safe.

Fraud Prevention Tips

- Use duplicate checks: These create a carbon copy every time you write a check, helping you track payments and spot fraud quickly.

- Report lost or stolen checkbooks immediately: Contact your bank right away to freeze your account or prevent unauthorized use.

- Set up account alerts: Many banks let you get SMS or email alerts for every check processed, so you stay updated.

Handling Bounced Checks

- Bounced checks happen if your account lacks funds or the check is invalid.

- Consequences include bank fees, penalties, and sometimes damage to your credit.

- To recover:

- Contact your payee promptly and arrange repayment.

- Ask your bank about overdraft protection to avoid future issues.

Advantages Over Digital Payments

- Personal checks don’t require a PIN, so there’s less risk of hacking through stolen codes.

- They offer a clear audit trail — every check is a physical, signed record you can track.

- Checks can sometimes be safer for larger or one-off payments where digital fraud is a concern.

Real-World Examples

- One case involved a person spotting a forged check quickly thanks to the duplicate copy, saving them from loss.

- In another, a bounced check led to quick overdraft protection setup, preventing future fees.

Ultimately, using wisely means combining smart habits with your bank’s tools to minimize risks and protect your finances.

Personal Checks Around the World: A Global Perspective

Personal checks have very different roles depending on where you are. In China, their use is quite limited. The country leans heavily on mobile payments and digital wallets like WeChat Pay and Alipay, making personal checks almost obsolete. There are still some pilot programs testing checks for business or government payments, but widespread adoption is low due to trust issues and the quick pace of digital finance. For now, personal checks remain a niche option in China.

In the U.S. and Canada, personal checks are more common, especially for rent, utilities, and certain bills. Immigrants often rely on checks because they might not have access to all digital banking tools yet. Banks here offer personal checking account setups that usually come with checkbooks, online access, and sometimes overdraft protection. Tips for newcomers include ordering secure checkbooks and using mobile banking apps alongside traditional checks to stay safe.

Emerging trends worldwide show a shift toward digital and e-check hybrids—checks issued and processed electronically—to combine the familiarity of checks with faster processing. Eco-friendly options are also on the rise, such as recycled paper checks and secure digital alternatives, helping reduce paper waste while keeping payment methods reliable.

Overall, personal checks vary in popularity and use, but digital trends are pushing them toward a more modern, secure future everywhere.

Sourcing Quality Personal Checks: Recommendations and Deals

When it comes to, quality matters a lot. Durable paper and secure printing aren’t just nice-to-haves—they protect your money and prevent fraud. Customization options like adding your name, logo, or special fonts can also make your checks look more professional and help avoid confusion.

Why Quality Counts

- Durable paper resists wear and tear, so your checks last longer.

- Secure printing features like watermarks, microprinting, and special inks reduce the risk of counterfeiting.

- Customization helps your checks stand out and can include your bank info, personal details, or even extra security codes.

Top Suppliers and Getting Started

Looking for trusted suppliers is key. Many banks offer check ordering services, but you can also find reputable third-party services online that often provide competitive deals and faster delivery. To start affordably:

- Compare prices between bank and third-party suppliers.

- Look for discounts on bulk orders.

- Check if there are deals for first-time buyers.

Single vs Duplicate Checks

- Single checks: You write, sign, and hand it out. Simple and cost-effective for occasional use.

- Duplicate checks: Create a carbon copy or electronic record every time you write a check. Great for keeping track of expenses without extra effort.

Laser vs Manual Checks

- Laser checks print details from your computer, ideal if you use accounting software.

- Manual checks are handwritten and usually less expensive, suitable for straightforward use.

Bulk Buying Tips

If you write checks often, buying in bulk can save money. Just make sure you:

- Only order what you realistically need to avoid unused stock.

- Opt for suppliers offering good customer service and easy reordering.

Sustainability Matters

Eco-conscious buyers should consider checks made from recycled materials. Some suppliers now offer green-certified paper and eco-friendly inks, helping to reduce environmental impact without compromising security or quality.

By focusing on these points, sourcing your personal checks can be smooth, affordable, and secure—perfect for keeping your finances in order.

FAQs: Answering Your Top Personal Check Questions

Here are some common questions about personal checks to help you feel confident using them:

How long is a personal check valid?

Usually, personal checks stay valid for about 6 months (180 days) from the date written. After that, banks may refuse to cash or deposit them.

Is it safe to mail a personal check?

Mailing checks is generally safe if you use secure envelopes and trusted postal services. To add extra safety, consider using certified mail or electronic payments when possible.

Where can I order the cheapest personal checks?

You can get affordable checks online directly from banks or trusted suppliers. Look for deals or bulk orders to save money. Just make sure the quality and security features meet your needs.

What should I do if I lose my checkbook?

Report the loss to your bank immediately to prevent fraud. They can stop any unauthorized checks and issue a new checkbook.

Can I use personal checks for rent or paying bills?

Yes, personal checks are still widely accepted for rent, utilities, and service payments. Just ensure you write them out clearly and keep a record for your budgeting.

How do I avoid bounced check fees?

- Always check your account balance before writing a check

- Enable overdraft protection if offered

- Use mobile banking alerts to track spending

If you have more questions or tips about personal checks, feel free to comment below. Sharing your experiences helps everyone handle checks smarter and safer!